Every pharmaceutical executive knows the phrase. Every investor fears it. Every generic manufacturer counts down to it. The patent cliff represents the precipitous drop in revenue that follows a drug’s loss of exclusivity (LOE) which is one of the most powerful, predictable, and paradoxically disruptive forces in the life sciences industry. This market shift occurs once a product loses its legal protection and triggers a sharp decline in earnings, making it one of the most powerful and predictable forces within the pharmaceutical industry.

And right now, the pharmaceutical world is staring down the steepest cliff it has seen since the early 2010s, when Lipitor, Plavix, and Singulair fell off the edge together. Between 2025 and 2030, blockbuster drugs worth hundreds of billions in annual sales will lose their patent shields and the scramble to respond is already rewriting pharma strategy at every level.

This article unpacks what the 2025 – 2030 patent cliff means: which drugs are falling, which companies are most exposed, and the IP strategies that will determine who survives and who thrives.

What Is a Patent Cliff and Why Does It Matter?

A patent cliff is not a metaphor for gradual erosion. It is a cliff a sudden, sharp drop in branded drug revenue, the moment generic or biosimilar competitors enter the market after patent expiry. On Day 1 of competition, a brand-name drug can lose 20 – 40% of its market share. Within 12 months, that figure routinely exceeds 80%.

The reason is structural. Patents grant pharmaceutical innovators a temporary monopoly typically 20 years from the filing date, though the effective commercial exclusivity is far shorter once you subtract the years spent in clinical development and regulatory approval. This exclusivity window allows companies to price drugs at a premium, recouping the enormous cost of R&D (which can exceed $1 billion per approved drug) and generating the profits that fund the next generation of innovation.

When that exclusivity ends, the economics flip violently. Generic manufacturers can produce chemically identical small molecules at a fraction of the cost, pricing them at 70 – 90% discounts. For biologics, biosimilars face higher development and regulatory hurdles but still erode brand market share significantly over time.

Case Study: Humira (adalimumab) and the Biosimilar Cliff

Humira, once the world’s best-selling medicine, offers a clear example of how quickly revenues can fall after loss of exclusivity. Following the end of U.S. patent protection and the 2023 entry of multiple lower-priced biosimilars, Humira’s U.S. sales declined sharply. Analysts have projected a further drop of roughly 37% in 2024 to about $13.7 billion, down from a peak of $21.2 billion in 2022.

- Biosimilar timing matters: when several launches cluster in the first year post-LOE, share erosion can accelerate.

- Net price pressure compounds volume losses as players rapidly shift formulary preference to lower-cost alternatives.

- Lifecycle strategies (new formulations, next-generation products, contracting) can soften but rarely eliminate the cliff.

- For portfolio planning, Humira underscores why replacing a single mega-blockbuster often requires multiple new launches.

Humira’s fall is not an anomaly. It is the template. And the 2025 – 2030 will produce many more such case studies on a scale.

The Drugs on the Edge: 2025 – 2029

The current patent cliff is widely considered the largest since the early 2010s wave from a lost-revenue standpoint. The US market alone is projected to forfeit over $230 billion in drug revenues between 2025 and 2030, with global estimates reaching $300 billion. Here are the most consequential expiries, year by year.

Drug (generic name) | Company | Therapy area | Est. LOE year | Peak revenue |

Eliquis (apixaban) | Bristol-Myers Squibb / Pfizer | Cardiology | 2028

| ~$12B |

Januvia / Janumet (sitagliptin) | Merck | Diabetes | 2026

| ~$5B |

Xeljanz (tofacitinib) | Pfizer | Immunology | 2028

| ~$2.5B |

Entresto (sacubitril/valsartan) | Novartis | Cardiology | 2025

| ~$7.8B |

Darzalex / Faspro (daratumumab) | Johnson & Johnson | Oncology | 2029

| ~$9B |

Opdivo (nivolumab) | Bristol-Myers Squibb | Oncology | 2029

| ~$9B |

Ibrance (palbociclib) | Pfizer | Oncology | 2027

| ~$5B |

Keytruda (pembrolizumab) | Merck | Oncology | 2028

| ~$25B |

Cosentyx (secukinumab) | Novartis | Immunology | 2029

| ~$5.5B |

Ozempic (semaglutide) | Novo Nordisk | Diabetes/Metabolic | 2031 (US; earlier ex‑US from ~2026) | ~$14-15B (2023) |

Jardiance (empagliflozin) | Boehringer Ingelheim / Eli Lilly | Diabetes/Cardiorenal | 2028–2030 (molecule earlier; later patents extend) | ~$13B |

Farxiga (dapagliflozin) | AstraZeneca | Diabetes / Cardiorenal | 2030 (US earliest broad generic) | ~$5-6B |

Tecfidera (dimethyl fumarate) | Biogen | Neurology (MS) | 2020 (generic launched after patent invalidation) | ~$4.6B |

Opdivo (nivolumab) | Bristol‑Myers Squibb | Oncology (PD‑1) | 2028–2029 | ~$9-10B |

Prolia/Xgeva (denosumab) | Amgen | Bone health/ Oncology supportive care | 2025 | ~$6.5-7B |

The single most significant expiry on this list is Keytruda, the world’s best-selling drug which faces patent challenge in 2028. At roughly $25 billion in annual sales, its LOE will represent one of the largest single revenue erosion events in pharmaceutical history.

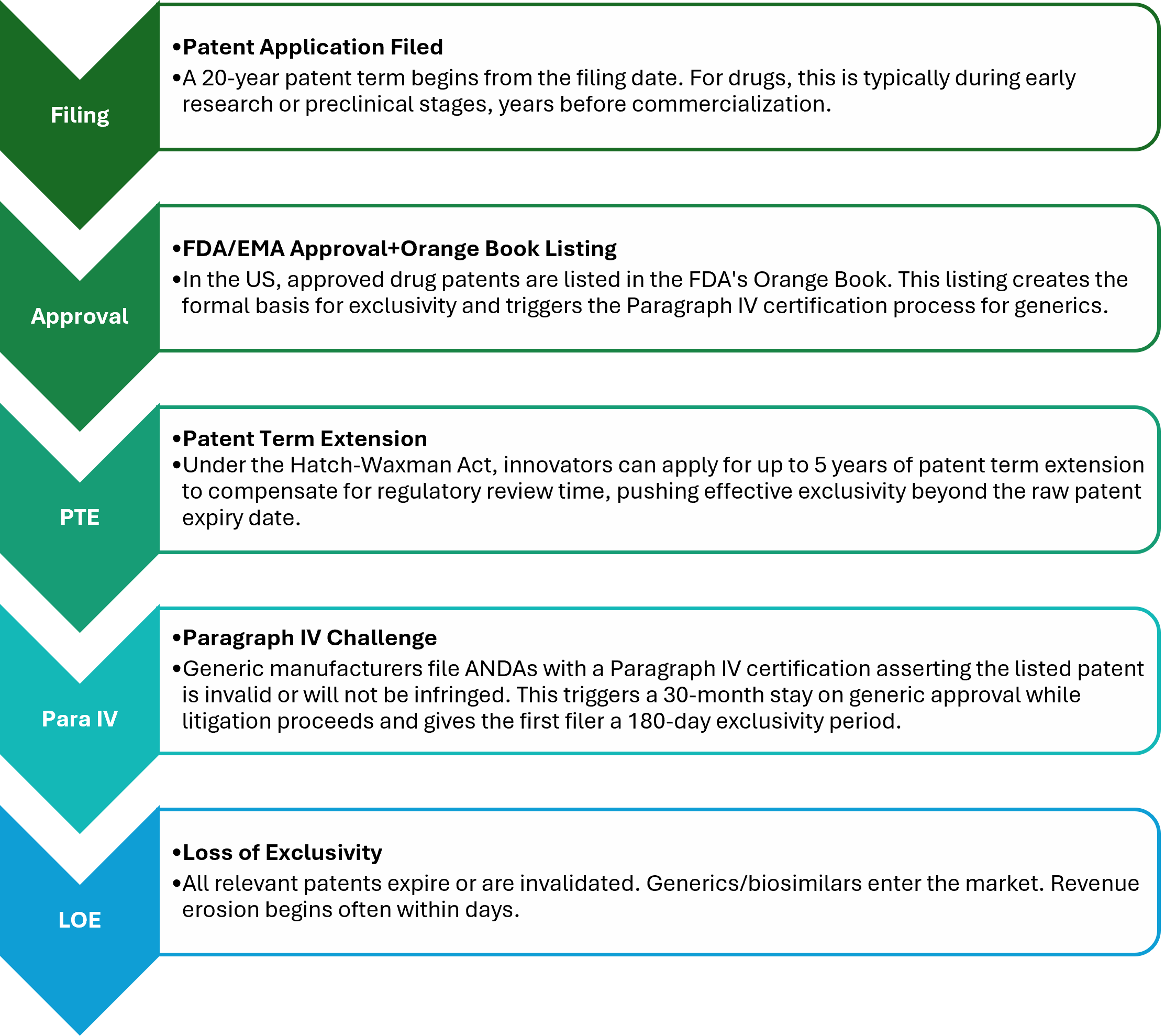

Patent Cliff’s IP Mechanics: What Actually Happens Legally?

For biologics, the process follows the BPCIA (Biologics Price Competition and Innovation Act), a more complex ‘patent dance’ framework that governs biosimilar applications. Biologics enjoy 12 years of regulatory exclusivity in the US regardless of patent status which partly explains why biosimilar uptake has lagged generics in terms of speed.

Strategic Implications for IP Practitioners

For patent attorneys, agents, and IP strategists working in life sciences, the current patent cliff environment creates both urgency and opportunity across several practice areas:

Prosecution Strategy

Companies with drugs approaching LOE should audit their entire patent portfolio composition, formulation, use, manufacturing, and device patents to identify enforceable claims that could delay generic entry. Continuation practice and divisional filings can strategically extend prosecution and keep relevant claim families pending.

Para IV Litigation

The volume of Paragraph IV certifications is rising alongside patent expiry dates. IP litigators should expect a surge in ANDA challenges targeting the drugs listed above. The 30-month stay mechanism remains a critical tactical tool for innovators but only if patents are robust, well-drafted, and timely listed in the Orange Book.

Freedom-to-Operate for Biosimilar Entrants

Biosimilar developers face complex FTO landscapes given layered patent thickets. Through clearance analysis covering cell lines, manufacturing processes, formulation, and method-of-treatment patents is essential before committing to development costs. The BPCIA patent dance creates procedural deadlines that require early legal engagement.

Biosimilar Interchangeability

The FDA’s interchangeability designation (allowing pharmacy-level substitution without physician sign-off) significantly accelerates biosimilar uptake. Regulatory patent strategy for biosimilar applicants should incorporate interchangeability filing timelines as a competitive differentiator.

Global Coordination

Patent cliffs are not US-only events. LOE timelines vary significantly across jurisdictions due to different patent term extension rules, regulatory data exclusivity periods, and litigation histories. IP teams managing global portfolios need jurisdiction-specific LOE calendars and coordinated lifecycle management strategies across the US, EU, Japan, and emerging markets including India and China.

Conclusion:

The 2025 – 2030 patent cliff is the most significant structural event in the pharmaceutical industry in over a decade. It will accelerate generic and biosimilar competition, intensify pricing pressures (particularly in oncology), drive a wave of M&A activity, and stress-test the pipeline strategies of virtually every major pharma company.

But cliffs, by definition, also reveal what lies below. For biosimilar developers, the revenue opportunity is generational. For biotech startups with differentiated assets, the appetite for acquisition has never been stronger. For patients, more affordable versions of critical medicines are finally within reach in categories long dominated by high-cost biologics.

For IP practitioners, the message is clear: this is not a passive environment. The next five years will require proactive portfolio management, sophisticated lifecycle strategy, and deep integration between patent teams and commercial strategy. The companies that navigate this cliff most skillfully will essentially transform their revenue profile through pipeline execution and will define the industry’s next chapter.

DISCLAIMER This article is intended for informational purposes in the life sciences IP community. It does not constitute legal advice. Patent expiry dates cited are based on publicly available reporting and are subject to change based on litigation outcomes, regulatory decisions, and patent term adjustments. Always consult a qualified patent professional for jurisdiction-specific guidance. |